In all the noise surrounding the latest market moves, political news and frenzy over tomorrow’s Fed rate hike (or pause), an important development was missed by many when Saudi Arabia released its budget for 2019 earlier on Tuesday, which at 1.106 trillion riyals, or $295 billion – the largest in the kingdom’s on record – represents a 7% increase from 1.030 trillion in 2018.

During the unveiling of the budget, Saudi King Salman said his country will continue paying public sector cost-of-living allowances for citizens and will boost spending to stimulate growth even as Saudi Arabia toils to close its deficit, which it won’t do yet again as the kingdom forecasts a 6th consecutive budget deficit in a row, estimated to hit $35 billion in 2019.

“We are determined to go ahead with economic reform, achieving fiscal discipline, improving transparency and empowering private sector,” the King said.

While state-funded Saudi “generosity” to keep its citizens happy – and not, say, thinking radical, revolutionary thoughts – is well known, analysts believe the continued cost-of-living allowances, first established in January 2018 and estimated by officials to cost more than $13 billion, are intended to stimulate sluggish growth but mostly shore up support for the royal family and Crown Prince Mohammed bin Salman after a controversy-ridden few months.

The royal allowances of 1,000 riyals a month ($266) are paid to civil servants and military personnel, and other allowances will continue for pensioners and those living on social security. Riyadh will also increase student benefits by 10 percent for the next fiscal year, the king announced.

There is just one problem: for Saudi Arabia to be able to meet its projected revenue and fund these generous payments it will need oil prices to rise higher. Much higher.

Looking at the details of the budget, a few troubling details emerge: revenue is forecast to hit 975 billion riyals while total spending will rise 7% to 1.106 trillion riyals, resulting in a 131 budget deficit, or 4.2% of GDP (nearly double the size of Italy’s projected deficit, if still quite smaller than the US deficit) as GDP is expected to grow from 2.3% in 2018 to 2.6% in 2019.

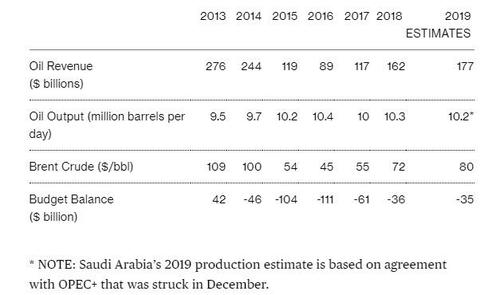

And while the government expects non-oil revenue to increase from 287 billion riyals in 2018 to 313 billion in 2019, the big question mark is what happens with oil revenue. According to the budget, Saudi Arabia expects oil revenues to grow nearly 10% from 607 billion riyals in 2018 to 662 billion in 2019, it is the assumptions embedded in this revenue forecast that are, well, concerning.

To hit 662 billion riyals in oil revenue, or $177 billion, up from $162 billion in 2018, Saudi Arabia expects near record oil output of 10.2 mmb/d sold at a price of $80/barrel, while Saudi Aramco won’t increase its allocations to the government. For reference, Brent settled just above $56 today, which means that oil has to rise at least 40% for the Saudi budget revenue assumption to be hit. Brent would have to rise an additional $15 to $95 a barrel for the kingdom to balance its budget deficit according to Bloomberg chief Middle East economist Ziad Daoud.

As a reference, analysts expect Brent in 2019 to trade around $73 a barrel, a number which may be rather aggressive considering the recent plunge in the commodity, largely the result of continued excess output coupled with declining demand from China and other key markets.

Even with these aggressive assumptions, which see Saudi Arabia oil revenue rising to a five-year high, the Kingdom will still post its sixth-straight budget deficit.

Last year, Saudi Arabia based its 2018 budget on crude averaging $63 a barrel, $17 below the latest forecast even as its OPEC-defecting neighbor, Qatar, assumed $55 per barrel in its budget forecast released last week.

So what happens if oil refuses to levitate to the desired price? As Bloomberg’s Javier Blas notes, “Saudi Arabia will need to take on further debt, spend its petro-dollar reserves or, at some point, introduce again austerity (as it was forced to do in 2015-2016).”

#SaudiArabia is anticipating fiscal #oil revenues in 2019 of ~$177 billion, compared with $162 billion in 2018 and the highest since 2014. That means the kingdom is betting on *much higher* prices for next year (assuming 10.2m b/d output from Jan 2019 as per #OPEC+ deal) #OOTT

— Javier Blas (@JavierBlas) December 18, 2018

It goes without saying that Saudi Arabia’s bullish call is the latest sign that the kingdom expects its efforts to corral OPEC members and its allies to cut production next year will support prices. On the other hand, any more Qatar-style defections, and the Saudi budget will not only be busted, but Saudi Arabia will end up taking on a lot more debt, which means it will be at the mercy of global creditors.

And while one can see an optimistic scenario in which everything goes as Saudi Arabia has planned, distinguished statistician and risk analyst, Nassim Taleb is not so sure, with a rather simple assessment: “Saudi Arabia is going to go bankrupt.”

https://twitter.com/nntaleb/status/1075150693718200321

Perhaps not just yet: according to the budget, public debt is expected to rise to 678 billion riyals or 21.7% of GDP, hardly an insurmountable number although, as noted above, it’s not the stock but the flow, and Taleb may well be right if Saudi Arabia’s traditional bankers decide to boycott the Kingdom, preventing it from gaining access to global capital markets, Taleb’s dour assessment may well be right.